I checked my bank balance this morning, as is my custom when I’m feeling a bit anxious and need a number to grab hold of.

I had £685.18.

Not too bad, considering it’s January, and I normally spend about a million pounds on Christmas. The rent has to come out still, but hey ho, not so bad.

And then I looked at that bit underneath that says ‘pending transactions’ – the things you’ve bought already, but just haven’t come out of your account.

Keeping it in the family this week, this post is written by Belle, aged 13. Thanks Belle!

So thanks to Osper, this year I am able to splash out on the people I love for Christmas!

I have planned the budgeting, the people I am getting the presents for and even ideas of what to get them. I am normally RUBBISH at budgeting as I normally spend it all in one go on a game or a new, random bit of junk that don’t need and will probably never use, but being able to see your balance anywhere makes you think a bit more about what you are going to buy.

I made lists, drew sketches, practised mind mapping and even had to do a lot of thinking! If you would like to see more then just watch the video below:

In my work as a digital marketing consultant* I’ve come across a lot of small businesses which have been given bad advice. It might be that they’ve had an agency managing their social media accounts, and they’ve not been happy with the results, or it could be that they’ve invested in a new website, only to discover it wasn’t really fit for purpose. All in all, it seems that running your own business can be a bit of a minefield.

(*I always feel very grown-up when I call myself that. It’s hard to reconcile that persona with the fact that last week I bought myself a plush grey and pink tortoise and called it Alan.)

It can actually be a very costly minefield, as being on the end of bad advice isn’t just a case of ‘Oh well, that didn’t work, what next?’ It can have a real impact on your business – financially and in terms of your reputation.

As the person giving the advice then, the pressure is on.

I’ve noticed a growing trend in the last couple of years for bloggers to start offering advice, particularly with things like web design and social media. This is great – it’s brilliant to see opportunities opening up for people to run their own businesses – but it also comes with risks.

Did you know for example, that customers could claim for compensation if they think your advice is negligent and has caused them a financial loss or damaged their reputation? Many clients may also ask you to provide proof of professional indemnity insurance before they work with you, especially if you’re working with local authorities or large companies.

If you provide a professional service, be it design, marketing, accountancy, IT, photography, or one of many other professions, it’s worth investing in professional indemnity insurance. This is the insurance that covers you should the worse happen, and your clients lose out due to any negligent advice or service you provide.

**Twitter party plug alert**

If you’re not sure about the types of insurance that your business needs, why not come along and join my Twitter chat on Tuesday 22nd September at 1pm?

Do you remember a little while ago I hosted a post from Jon at The Money Shed about ways to earn money from home? Well, I have another post from Jon today – and easy matched betting how to guide. I’ve had a go to test the theory, and it worked, but Jon is an expert at matched betting and makes thousands! Why not give it a try and let me know how you get on? (Be careful and cautious with your money of course.)

Hi everyone – Jon again here from The Money Shed, the UKs largest community website for earning money from home.

I believe it was 90s one hit wonder artist Betty Boo who announced her arrival with the profound lyric “it’s me again, yes, how did you guess? ‘Cause last time, you were really impressed”

Indeed the last time I guest posted on this fantastic blog I told you 4 ways to earn over £600 a month from home and now I’m back with 1 way for you to earn over £1000 a month AND it’s TAX FREE. It’s called matched betting. It’s easy to do, 100% legal, very easy to follow and will have you earning some serious cash in as long as it takes you to make a bet online. It’s also worth mentioning that all this is RISK FREE. You will not lose money doing matched betting – it is not betting in the traditional sense. Basically you earn money by taking advantage of all the free bet offers that bookies give out and harnessing GUARANTEED PROFIT from them.

I’ve been personally doing matched betting for the last 5 years and have earned over £40,000 so far (Which I’ve detailed on our Matched Betting Guide).You can do this even if you have never placed a bet in your life!

In this post I’m going to do give you enough of an understanding of how Matched Betting works so you understand the basics and should set you on the path to earning some major money from home. If you are after a more detailed guide then take a look at our 7000+ word Beginner’s Guide to Matched Betting.

To get you in the mood, here’s a very short video to set the scene:

I am going to make you around £15 with zero risk in the next few minutes so listen closely.

The bookie we will be using is Coral and the exchange we will be using is Betfairso click through to both of those and make your setup your accounts now so that everything is ready for your to use!

Our Qualifying Bet – OK, it’s time to get our hands dirty. Bookies offer free bets all the time to both new and existing customers. Usually to get those free bets you need to do something like bet £20 and get a £10 free bet free. If you were betting normally there is a chance you might lose your £20 on your qualifying bet just to get access to the £10 free bet. We are going to overcome that problem by laying (betting against our bets) at the exchange (betfair).

Coral have a very simple and easy to follow sign up offer.

Bet £5 and get a £20 free bet.

To qualify for this £20 free bet we need to place a £5 bet at odds above 1.5. When we are doing matched betting we work in decimals so if you look at the VERY top of the coral website you will see you can select to use decimal – click that first.

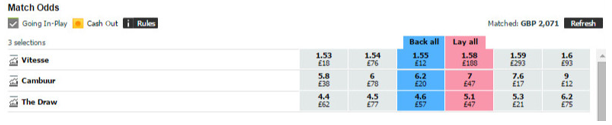

In this example I am going to be using my £5 qualifying bet on Vitesse vs Cambuur. As you can see below the odds of Vitesse to win are 1.5 so this is perfect.

We now need to open up Betfair and go to their exchange to bet AGAINST this win from happening. That way no matter what the outcome we won’t have lost our full £5.

Login to BetFair, click on EXCHANGE at the top and use the little search bar at the top to search for the team / horse / whatever you are betting on.

Once you find it you should get a screen that looks a bit like this:

The pink section is all we care about on the exchange. Just to help you out a bit here, when we BACK an event at the bookie (ieVitesse are going to win) we always LAY it at the Exchange (ieVitesse are NOT going to win and will either lose or draw). We then have every eventuality covered.

As you can see the odds for laying Vitesse are 1.58. Ideally we want our odds to be as close together as possible so this isn’t a bad match at all.

Before we place our back and lay bet we need to use a special matched betting calculator. There are lots around but I find TrickyBet is a good one to use. Open up the calculator are we need to enter a few numbers.

FOR MY EXAMPLE:

The Bet Type is Normal

The Bet is £5

The Back odds are 1.5 (You would enter your OWN odds here normally)

The Lay odds are 1.58 (You would enter your OWN odds here normally)

The Lay Commission needs to be set at 5% as that is the commission that Betfair charge for using their exchange.

Press Calculate and your calculator should now look something like this (although obviously with YOUR odds in it):

By looking at the bottom we can see we are going to make a very small 34p loss doing this qualifying bet. That is ACCEPTABLE as we will be making our money with the free bet. We nearly ALWAYS make a very small loss on the qualifying bet – we only do the qualifying bet to get access to the free bet.

Go back to the coral website and now place £5 on your chosen bet (in this case Vitesse)

Deposit around £10 into Betfair and now place your lay bet. Simply click on the pink Lay odds for your chosen bet and put in the value that the calculator tells you to which is this case is £4.90

Out qualifying bet is now done. No matter what the outcome we will have made a 34p loss, it doesn’t matter if the bet wins at the bookie or wins at the exchange.

After the event has happened (or sometimes as soon as you have placed your qualifying bet) you will get given a £20 FREE BET from Coral. Now it is time for us to make our money.

Here we can go for whatever odds we want, I would suggest something around 4.0/5.0/6.0 as you won’t need too much money in the exchange then.

Find a race / match that offers odds on the coral website of 4.0 or above.

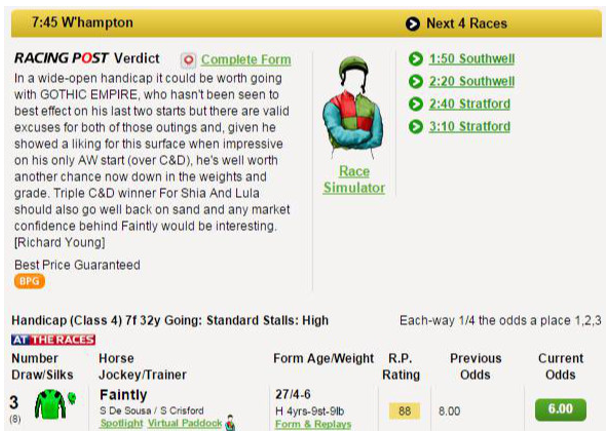

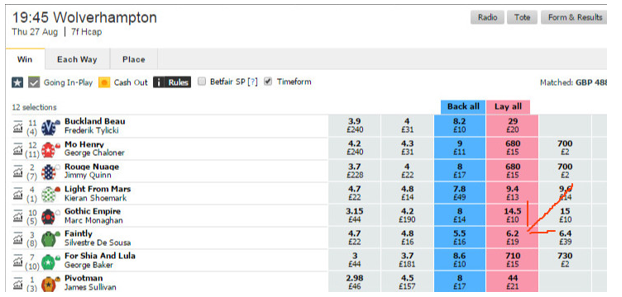

For this example I have decided to bet on a horse called Faintly with odds of 6.0 in the 7pm race at Wolverhampton:

When I look him up on Betfair I see his lay odds are 6.2:

So we have all the figures we need and now it’s back to the TrickyBet calculator.

FOR MY EXAMPLE

The Bet Type is SNR (Stake Not Returned)

The Bet is £20 (This is the value of our free bet)

The Back odds are 6 (You would enter your OWN odds here normally)

The Lay odds are 6.2 (You would enter your OWN odds here normally)

The Lay Commission needs to be set at 5% as that is the commission that Betfair charge for using their exchange.

So as we can see we are going to make £15.45 profit (which minus our 35p loss from the qualifier is £15.10). We have done this in the time it takes us to place 2 bets and it is GUARANTEED PROFIT

Next we need to go back to coral and place our £20 free bet on our chosen horse. Once you select it on the right you will get an option to select to ‘Use your free bet’ simply choose it and put £20 on your chosen event.

Over at the exchange (Betfair) I am going to lay £16.26 just like it is telling me to. I need a liability of £84.55 so deposit some more money into Betfair if you need it. Liability is just BetFairs way of wanting a small guarantee for your lay bet as the chances of 1 horse NOT winning the race is FAR higher. Don’t worry, you will either win at the bookie or the exchange again so you won’t be out of pocket.

And that’s IT!

If you follow those instructions you will have made £15 for a few minutes work – totally RISK FREE and TAX FREE as you don’t pay tax on UK Gambling winnings.

So, how do you go from £15 to £1000 a month – VERY EASILY.

What I’ve just shown you is just the mechanics of Matched Betting. Basically I am just showing you how it works and how you can make money from it. What you really need is a Matched Betting service that can spoon speed you offers each and every day with full instructions and idiot proof video guides showing you what to click and where when placing your bets.

If you’re the sort of person who likes to make an informed decision, The Money Shed Blog has both an in-depth Profit Accumulator Review and OddsMonkey Reviewthat compares the two main matched betting services in the UK with extremely detailed reviews to help you choose one that is going to give you what you want for your budget.

If you want to just crack on, one very decent service is Profit Accumulator

The Matched Betting service I recommend above ALL OTHERS is without doubt Profit Accumulator. Profit Accumulator is a Matched Betting service which like I mentioned basically feed you an endless stream of offers from the bookies that you can take advantage of. Instead of having to go out and find them yourself you simply login to their website and you are presented with a link for each bookie free bet offer available which gives you not just instructions on how to do the offer but also a video showing you what to click on.

Profit Accumulator offers a range of services for betting, helping you to find the greatest offers for you and the best ways to win big. This site can be used with both betting and bingo sites such as www.boomtownbingo.com and works fantastically across many different platforms. Profit Accumulator has over 20,000 users worldwide, and boasts an excellent dedicated support system that are focused on providing the best service for you.

You also get access to a fantastic bit of software called ‘OddsMatching’ which lets you select a bookie from a drop down list and filter the bets. So if you wanted to find all the bets available ABOVE 4.0 on Coral. Instead of manually having to find them you just go to the OddsMatching page, choose coral from the drop down list and enter 4.0 into one of the filter boxes and you get presented with all available bets and links directly to them. It saves you a huge amount of time and lets you just get on with earning money as quickly as you can.

If you are already an existing member with a number of high street bookies don’t worry about it, new free bet offersfor existing customers with different bookies appear every few days throughout the week and Profit Accumulator will direct you to those as well as it is updated throughout the day. With the football season having just started again there is MAJOR money to be made with Matched Betting as the likes of Paddy Power and Skybet regularly offer Bet £20 get £10 type deals on every match that is shown on Sky/BT at the moment. There is SO MUCH MORE to matched betting in terms of what you can earn but I just wanted to give you a small taste and show you that is possible to make money from it.

If you want to sign up to Profit Accumuator it costs £17.99 a month, with that price going down to £14.99 after a year, or £150 a year (don’t worry about those costs as you will make MORE than the money you need to pay for it without question). They also offer a FREE TIER membership where you can earn £45 TODAY from offers they present you with and then you can either take you £45 and leave or pay them some money to get access to their services.

Hopefully this post has made some sense to you. If you have any questions then just leave a comment below and I will help out as best you can and if you are looking for other ways to earn money then make sure to check out our ever popular 20 Work from home jobs for Mums and How to Get Money Fast blog posts which cover over £5000+ in income for you to earn from home! For something that’s more about fun that guaranteed income, try a promo code for Text 888Ladies.

Looking for new ways to earn decent money online? Thanks to Jon from The Money Shed for this guest post. It’s not a sponsored post or anything, we just got chatting after I wrote my post about 43 ways to get more blog traffic, and we thought it might be useful. I’ve not tried any of these methods myself, so can’t vouch for them, but I’d be interested to know if you have or, if you do, how you get on. Enjoy!

I EARN £1000s FROM MY BEDROOM – WANT TO FIND OUT MORE?

CLICK HERE!

This is how earning money from home is usually introduced to the majority of people. They click on the magical words, expecting to learn how they can earn that sort of money from their bedroom, and are typically then introduced to one of the many MLM, (Multi level Marketing), companies out there, such as Younique / Avon / Forever Living or even worse, survey sites!

This month saw the arrival of my second post-Christmas credit card statement. I felt rather pleased with myself opening it, because I knew that even though I accidentally spent about £1,500 on it on Christmas presents, I paid off the balance almost completely in the first week of January.

*looks smug*

So self-satisfied was I in fact, that I almost wanted to punch myself in the face.

My eye was caught though by the line telling me I had ‘£13,416 available to spend’.